Let’s Talk … About the Power of Compound Returns

Building a strong retirement fund doesn’t always require large contributions upfront—it starts with consistent saving and benefits from the power of time. Compounding returns can let your money grow exponentially by earning returns not just on your initial investment, but also on the returns those investments generate. The earlier you start, the more your savings has the potential to multiply, turning small contributions into a substantial nest egg over the years.

How Does It Work?

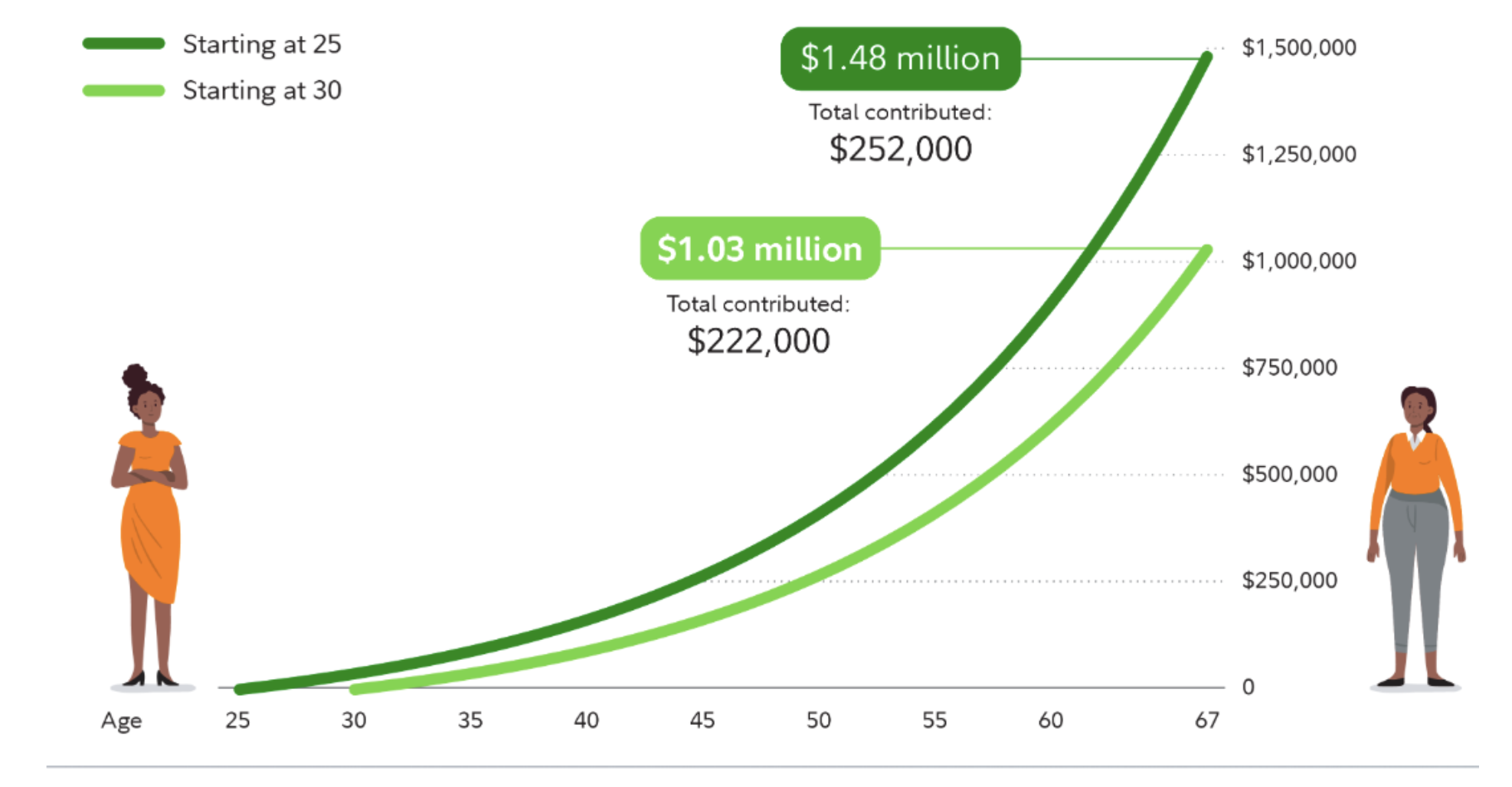

Compounding returns create a snowball effect: your investment gains generate their own returns, amplifying growth over time. Fidelity illustrates how starting early versus waiting can affect retirement savings:

Imagine two savers each contribute $6,000 at the start of every year until they retire at age 67. The difference is one starts at age 25, while the other starts at age 30. Both earn an average annual return of 7%. By retirement, the person who started at age 25 sees their savings grow to about $1.5 million, while the person who started at age 30 has a balance of just over $1 million—a difference of nearly $500,000. What’s striking is that the person who started at age 30 invested only $30,000 less over the years but ended up with nearly $500,000 less at retirement, showing how just five years of earlier saving can make a huge difference thanks to the power of compounding returns. Of course, this is just an example, and losses can also occur.

Source: Fidelity

Consistency Over Size

Saving in small, steady steps can have a meaningful impact due to compounding. You don’t need a large amount to start; the real power comes from time and ongoing contributions. Regularly adding to your investment, even in modest amounts, can let your balance grow year after year. Tax-advantaged accounts—like 401(k)s and traditional IRAs—help earnings stay invested longer by growing tax-deferred, so more of your money remains in the market. And because money left invested has more time to compound, starting early can multiply the effect. For more on this, read “Let’s Talk About…Why Starting to Save Early Matters.”

Practical Tips to Grow Your Savings

- Explore the Halliburton 401(k) plan options: Investing your savings wisely is key to maximizing compounding returns. The Halliburton 401(k) plan offers a variety of investment options tailored to different risk tolerances and goals. Whether you prefer ready-made Retirement Portfolios or want to customize your investments with Single Focus Strategies, choosing the right mix could help your money grow steadily over time. To learn more, read “Let’s Talk…About Investing for Beginners”.

- Use dollar-cost averaging: Consider investing a fixed amount regularly to buy more shares when prices are low and fewer when prices are high. This smooths out market volatility and reduces risk.

- Prioritize consistency over timing: Trying to time the market is risky. Staying invested and contributing regularly helps you capture more of the market’s good days.

- Turn time into progress: Even modest contributions made early can yield larger payoffs than larger contributions made later.

Let the Halliburton Annual Increase Program Do the Work for You

The Annual Increase Program automatically raises your contribution rate by 1-10% annually, on the date you choose. This automatic increase is a quick and easy way to set yourself up for success in saving for retirement. You can view or change your Annual Increase Program election anytime.

Everyday Tips to Maximize Compounding Returns

Start with what you can afford: Even if you can only save a small amount now, start today. The power of compounding means your money has more time to grow.

Increase contributions gradually: Fidelity research shows that increasing your contribution by just 1% annually can make a meaningful difference over time. To see how much, check out Fidelity’s Power of Small Amounts tool.

Avoid dipping into your savings: Resist the temptation to withdraw from your retirement accounts early. Keeping your money invested allows compounding to work its magic, and allows you to avoid early withdrawal penalties.

Review and adjust your investments: Periodically check your investment mix to ensure it aligns with your goals and risk tolerance. A well-diversified portfolio can help manage risk and support steady growth.

Compounding returns reward patience and consistency. By making regular contributions and giving your savings time to grow, you’ll increase the potential for a richer, more secure retirement. Start today, stay consistent, and watch your savings grow!

Sources:

Fidelity: The Power of Compounding Plus Regular Investing

Fidelity: What is Compound Interest?

Investopedia: The Power of Compound Interest: Calculations and Examples